Recession talk is all over the news, and the odds of a recession are rising this year. And that leaves people wondering what would happen to the housing market if we do go into a recession.

Let’s take a look at some historical data to show what’s happened in housing for each recession going all the way back to the 1980s.

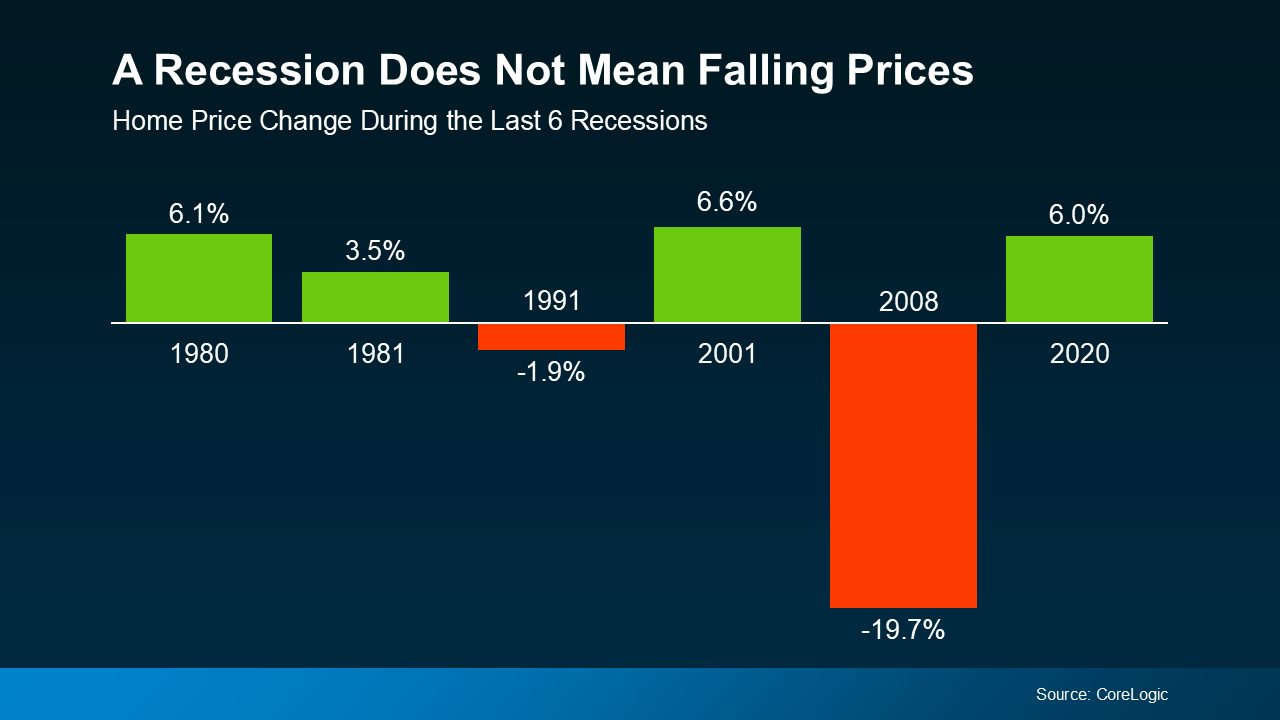

Many people think that if a recession hits, home prices will fall like they did in 2008. But that was an exception, not the rule. It was the only time we saw such a steep drop in prices. And it hasn’t happened since.

In fact, according to data from CoreLogic, in four of the last six recessions, home prices actually went up (see graph below):

So, if you’re thinking about buying or selling a home, don’t assume a recession will lead to a crash in home prices. The data simply doesn’t support that idea. Instead, home prices usually follow whatever trajectory they’re already on. And right now, nationally, home prices are still rising at a more normal pace.

So, if you’re thinking about buying or selling a home, don’t assume a recession will lead to a crash in home prices. The data simply doesn’t support that idea. Instead, home prices usually follow whatever trajectory they’re already on. And right now, nationally, home prices are still rising at a more normal pace.

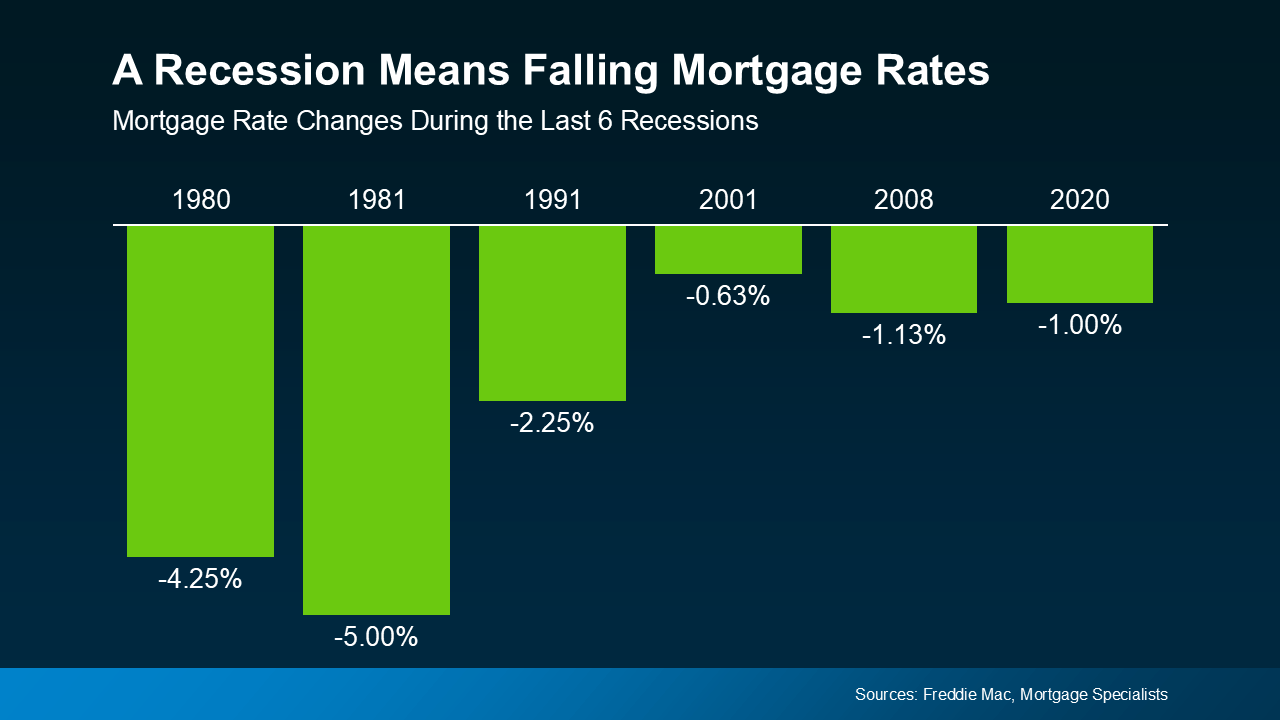

While home prices tend to stay on their current path, mortgage rates usually drop during economic slowdowns. Again, looking at data from the last six recessions, mortgage rates fell each time (see graph below):

So, a recession means mortgage rates could decline based on the data. While that would help with affordability, don’t expect the return of a 3% rate.

So, a recession means mortgage rates could decline based on the data. While that would help with affordability, don’t expect the return of a 3% rate.

The answer to the recession question is still unknown, but the odds have gone up. But that doesn’t mean you have to wonder about the impact on the housing market – historical data tells us what usually happens.

When you hear talk about a possible recession, what concerns or questions come to mind about buying or selling a home?

Retirement isn’t just a milestone. It's the beginning of something really special. After years of hard work, it’s finally time to slow down, explore new passions, and live life on your own terms.

But with this exciting chapter comes some big choices. And one of the biggest is this: does your current home still make sense for the lifestyle (and budget) you want in this next phase of life?

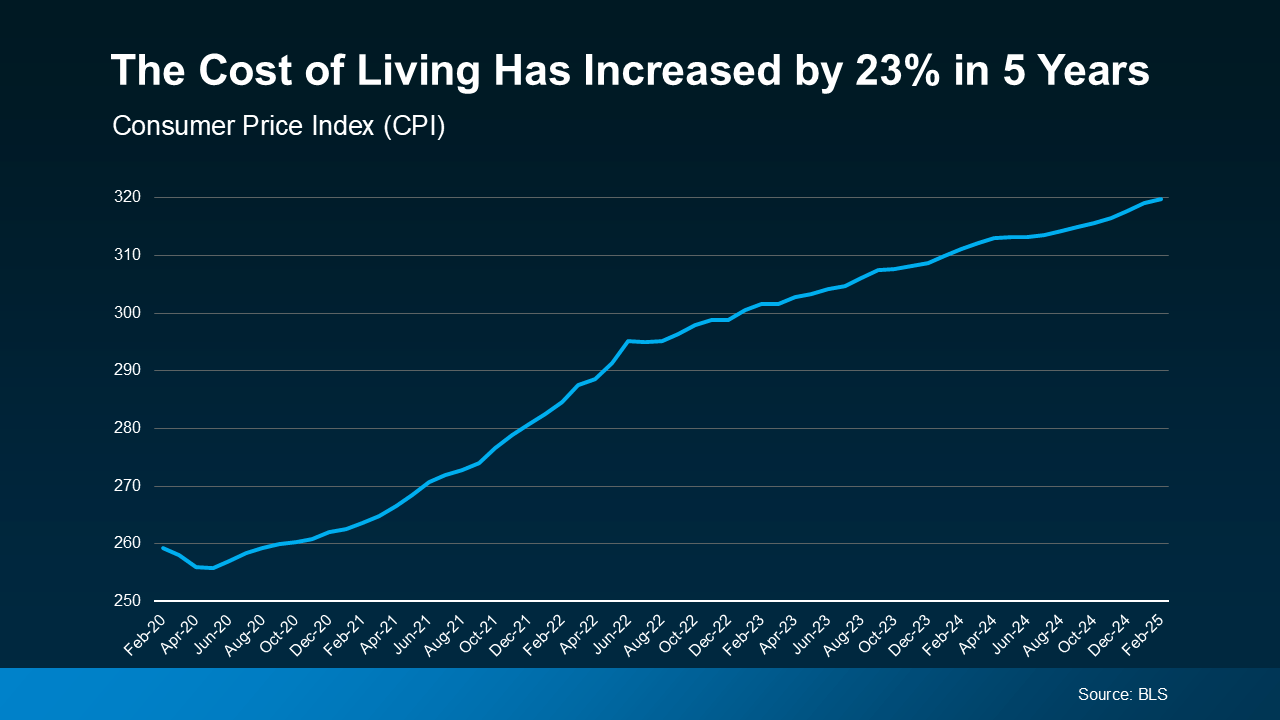

That’s an especially important question right now. Just in the past five years, the cost of living has jumped by 23% according to the Bureau of Labor Statistics (BLS). That’s based on the Consumer Price Index (CPI), which is how changes are tracked in the average price consumers pay for goods and services (see graph below):

When you’re thinking about how to make your retirement savings last, those rising expenses matter. And if you’ve started to wonder whether your money will stretch as far as you need it to go, don’t worry. You may have more control than you think.

When you’re thinking about how to make your retirement savings last, those rising expenses matter. And if you’ve started to wonder whether your money will stretch as far as you need it to go, don’t worry. You may have more control than you think.

One way many retirees are protecting their savings is by relocating. Because your dollars do go further in some places.

Moving to an area with a lower cost of living can help you save on regular expenses like your housing, utilities, and taxes – especially if you downsize at the same time.

And that can free up room in your budget for the things that make retirement some of the best years of your life: travel, hobbies, spoiling your grandkids, or any of the other things you’ve been dreaming about doing in this next phase.

That’s not to say you have to move. It just means you’ll want to think about where you plan to live and make sure you’ve got enough savings to cover actually living there. It's all about planning. As Go Banking Rates explains:

“How much you should have saved for retirement depends on a few key factors, including your location. Where you choose to spend your golden years is critical.”

And you don’t always have to go far. Sometimes it’s out of state, but other times moving to the suburbs instead of living near the city can make a big difference. And that’s worth thinking about as you plan for your next chapter.

Whether you’re considering downsizing, moving closer to your grandkids, or heading to an area where you can stretch your savings, a real estate agent can help. They’ll work with you to explore the options that make sense for your goals – and can help make selling your current house easier. They can also connect you with trusted agents in other parts of the country if you're considering a big move.

You’ve worked hard to build a future you can enjoy. If your current home or location no longer supports that, it may be time to explore what’s next.

What does your ideal retirement look like? And could a move help make it even better? Connect with an agent to talk about how to make that vision a reality.

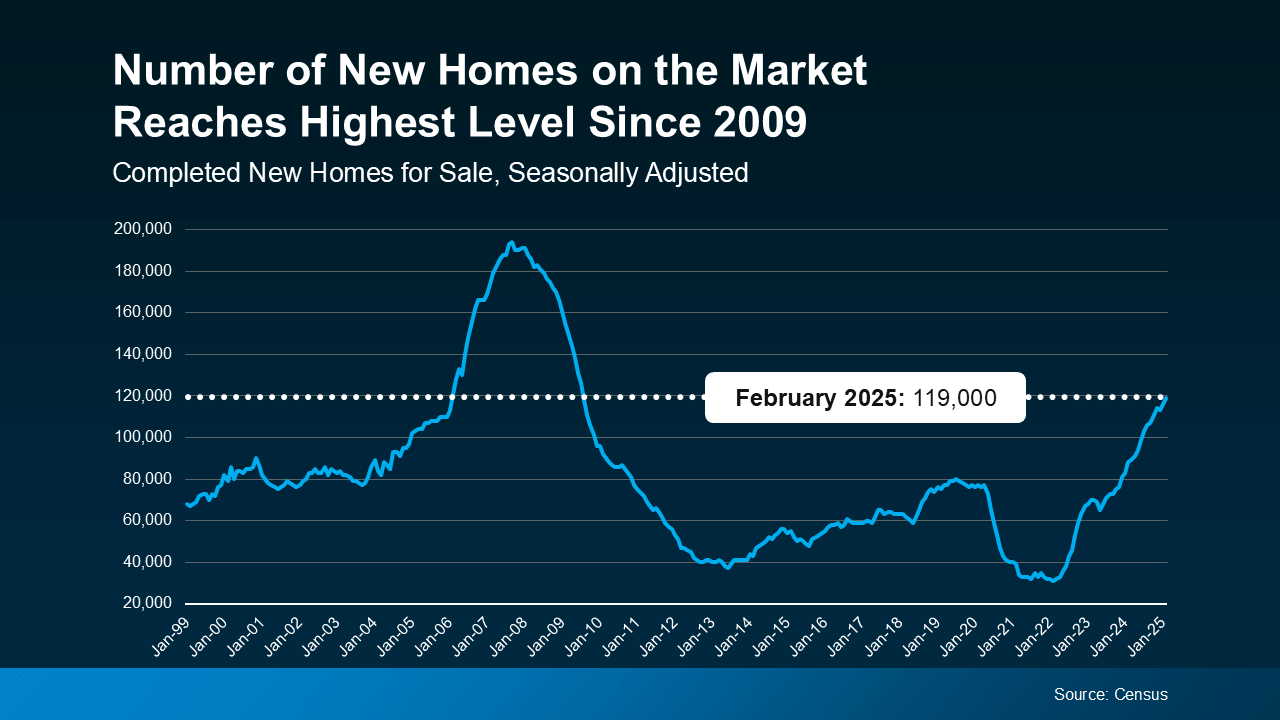

Headlines are talking about the inventory of new homes and how we’re back at the levels not seen since 2009. And maybe you’re reading that and thinking: oh no, here we go again. That’s because you remember the housing crash of the late 2000s and you’re worried we’re repeating the same mistakes.

But before you let fear take hold, remember: headlines are designed to be clickbait. And a lot of the time, they do more to terrify than clarify. That’s because they don’t always give you all the context you need. So, let’s take a step back and look at what the data really says.

While it’s true the number of new homes on the market has reached its highest level since 2009, that’s not a cause for alarm.

Here’s the context that matters most. When the data is turned into a graph, it’s clear the amount seen in 2009 wasn’t the peak of oversupply – not even close. That high point came earlier in 2007-2008. If anything, 2009 was when the number of new homes being built was really starting to slide back down (see graph below):

The overbuilding that contributed to the housing crash happened in the years leading up to 2008. Not in 2009. At that point, construction was already slowing down. So, saying we’ve hit 2009 levels isn't the same thing as saying we’re overbuilding like we did the last time.

The overbuilding that contributed to the housing crash happened in the years leading up to 2008. Not in 2009. At that point, construction was already slowing down. So, saying we’ve hit 2009 levels isn't the same thing as saying we’re overbuilding like we did the last time.

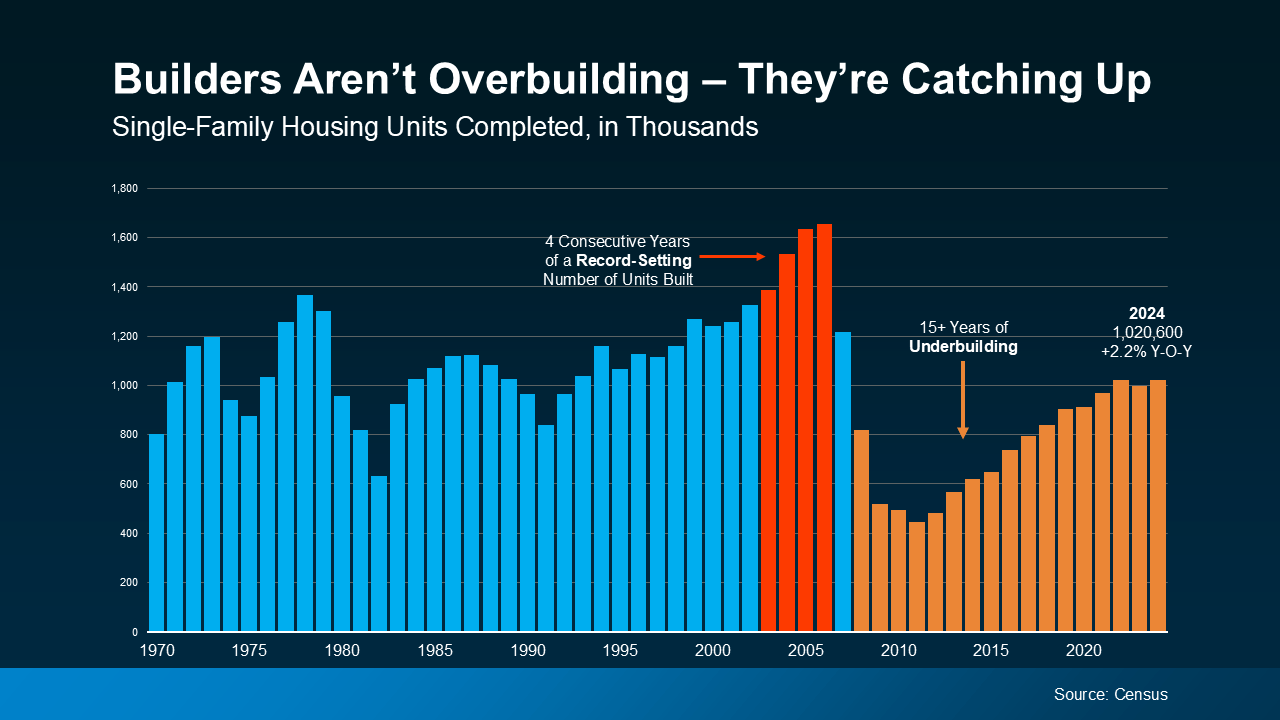

Here’s some more data to prove it to you. After the crash, builders pulled production way back. As a result, they built far fewer homes than the market needed. And that was a consistent problem that lasted for over a decade. That long stretch of underbuilding created a major housing shortage, which is still a challenge today.

The graph below uses Census data to show the number of new homes built each year over the past 52 years. You can clearly see the overbuilding leading up to the crash (in red), the period of underbuilding that followed (in orange), and how we’re only now getting back to a more normal level of construction:

Today’s situation is different. Builders aren’t overbuilding – they’re catching up.

In a recent article, Odeta Kushi, Deputy Chief Economist at First American, highlights this deficit and speaks to why the recent ramp-up in construction is actually good for today’s market, especially buyers:

“This means more homes on the market and more options for home buyers, which is good news for a housing market that has been underbuilt for over a decade.”

Of course, like anything else in real estate, the level of supply and demand will vary by market. Some markets may have more newly built homes, some less. But, nationally, there’s nothing to worry about. This isn’t like the last time.

No matter what you’re reading or seeing, the growing number of newly built homes on the market isn’t a red flag nationally – it's a sign builders are starting to make up for years of underbuilding. If you want to talk about what’s happening in your market, connect with an agent.

If you’ve been frustrated by the lack of homes for sale over the past few years, here’s some good news. You have more options, so it may finally be time to kick off your home search again. As Daryl Fairweather, Chief Economist at Redfin, explains:

“Now is the best time to buy in the last two years. Mortgage rates are comparable to what they were two years ago, and prices remain high. However, there is significantly more inventory . . .”

The number of homes for sale has grown compared to last year, and even more options are on the way. While this is typical for the busy spring season, here’s why this is so important right now.

Homeowners are listing their houses at the highest pace we’ve seen in a while.

Over the past few months, the number of new listings, or homes that have recently been put on the market for sale, has been steadily rising (see graph below):

Basically, more people are putting their homes on the market each month – whether they’re moving up, downsizing, or relocating. And this trend is a positive sign for the housing market.

Basically, more people are putting their homes on the market each month – whether they’re moving up, downsizing, or relocating. And this trend is a positive sign for the housing market.

Sellers who may have been on the fence the past few years are starting to jump back in. That’s helping to boost overall inventory and create better opportunities for both buyers and move-up sellers alike.

But it’s not just that the number of fresh options is up month-over-month; there’s also been a jump compared to last year.

According to Realtor.com, new listings in March were 10.2% higher than last year, making it the biggest March for new listings since 2021 (see graph below):

For anyone who’s been waiting for more choices, this is exactly what you’ve been hoping for – because more homes coming onto the market means more options and a better shot at finding one that fits your needs.

For anyone who’s been waiting for more choices, this is exactly what you’ve been hoping for – because more homes coming onto the market means more options and a better shot at finding one that fits your needs.

To make sure you don't miss out on any of the latest listings for your area, lean on a local real estate agent.

If you're thinking about making a move this spring, now may be the time to start exploring your options. With more fresh listings hitting the market, you may find a home you love waiting for you.

What features or neighborhoods are at the top of your wish list?

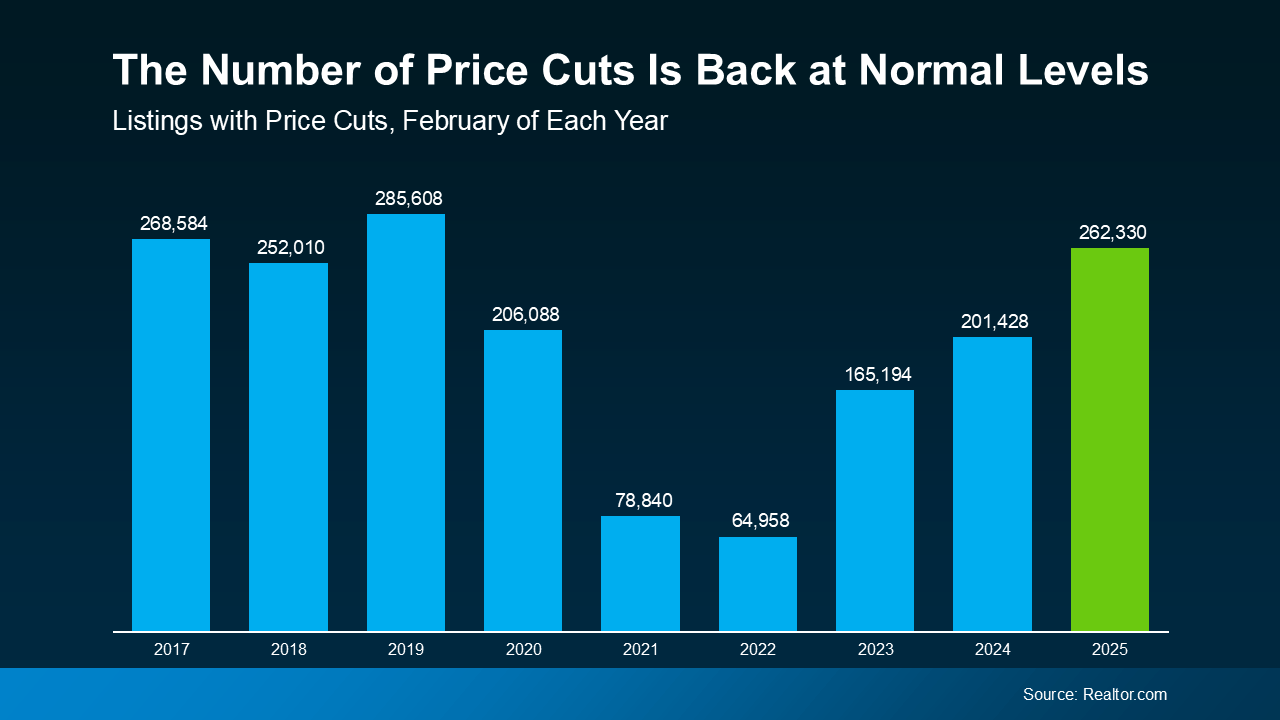

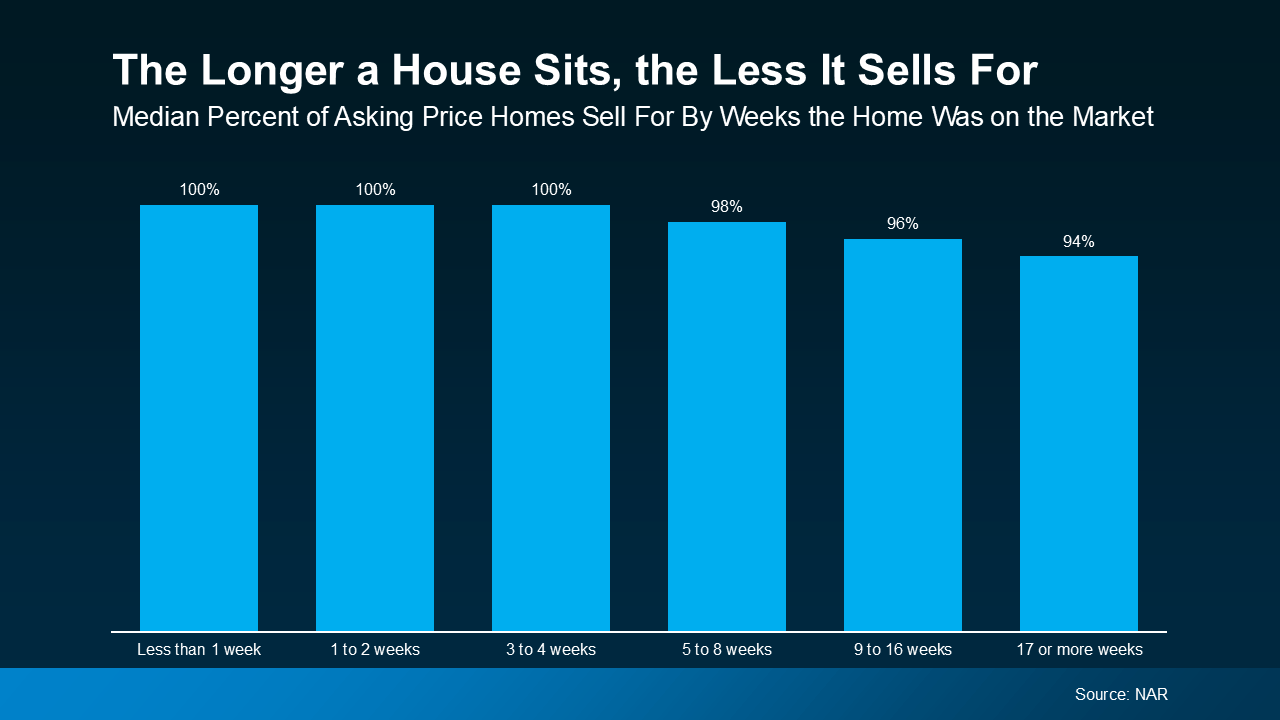

When you put your house on the market, you want to sell it quickly and for the best price possible; that's generally the goal. But too many sellers are shooting too high right now. They don’t realize the market has shifted as inventory has grown. The side effect? Price cuts are on the rise, but they really don’t have to be. Here’s why.

According to data from Realtor.com, in February, price cuts were the highest they’ve been in any other February since 2019 (see graph below):

If you consider that 2019 was the last true normal year for the housing market – that's a big deal. We’re getting back to what’s typical for the market.

This isn’t the same frenzied seller’s market we saw a few years ago. You may not get the same price your neighbor did at the height of the pandemic. And that means you may need to reset your expectations.

Because here’s the reality. If you shoot too high and have to lower your price after the fact, you could actually end up walking away with lower offers than if you’d priced it right from the start. So, how do you avoid that? You lean on your agent.

A great agent doesn’t just pull a number out of thin air. They’ll use real data and market trends to make sure your house is priced based on what your specific home is valued at today. So, you’re setting a realistic price – one that’ll draw in serious buyers.

And based on your agent’s analysis of your local market, they may even recommend strategically pricing slightly below market value to help your house attract more eyes and more competitive offers. Here’s how your agent will determine the right number for your house:

Unfortunately, some sellers still ignore their agent’s advice and prefer to start high just to see what happens. The hope being maybe they get their full asking price, or they at least have more wiggle room for negotiation. But pricing high usually ends up costing you, and here’s why:

You can see that shake out in the graph below. It uses data from the National Association of Realtors (NAR) to show that the longer a house sits, the less it’ll sell for:

This graph shows that if a house sells within the first 4 weeks it is listed, it usually goes for full price. Based on experience, that's what usually happens to homes that are priced at or just below current market value. If it’s priced right, buyers will be interested, and, ultimately, willing to pay the asking price – or compete with other buyers and even go over asking.

This graph shows that if a house sells within the first 4 weeks it is listed, it usually goes for full price. Based on experience, that's what usually happens to homes that are priced at or just below current market value. If it’s priced right, buyers will be interested, and, ultimately, willing to pay the asking price – or compete with other buyers and even go over asking.

But if a house isn’t priced right, it doesn’t sell as quickly. And this graph shows that, after the first 4 weeks on the market, the price starts to drop from there. That’s because buyer interest falls off the longer it sits. So, it becomes more likely a seller will either accept a lower offer because that’s all they have, or opt to do a price drop to draw people back in.

The last thing you want is to list too high, watch your house sit, and then have to drop the price just to get attention. Talk to a local agent so that doesn’t happen to you.

Want to make sure your home sells quickly and for the best price? Connect with an agent to talk about the right pricing strategy for your house.

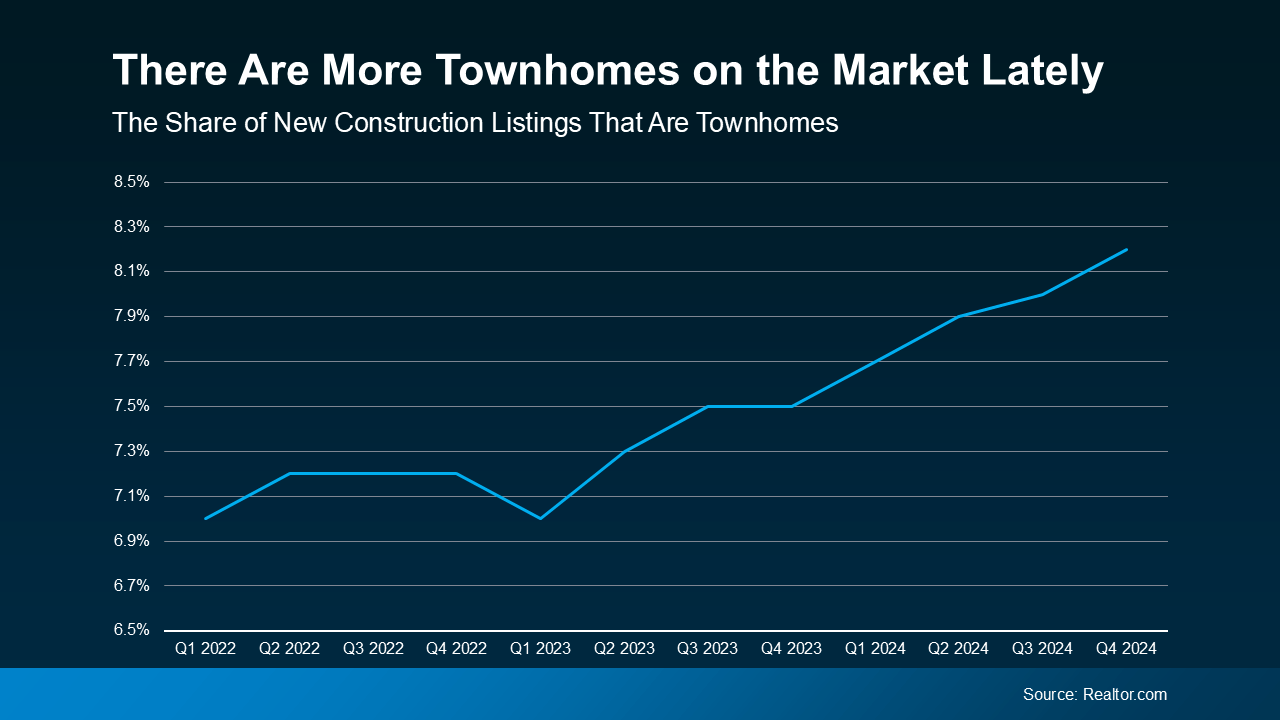

Buying your first home in today’s market can feel tough. Between high home prices and mortgage rates, affordability is still a big challenge. And some buyers are making one simple trade-off that’s getting them in the door faster: square footage.

According to the National Association of Home Builders (NAHB), 35% of buyers are willing to purchase something smaller to make homeownership happen. And one place you can usually find a smaller footprint (and sometimes better affordability) is in townhomes.

Townhomes typically cost less than single-family homes due to their more limited size. And that’s a big plus for today’s budget-conscious buyer. As Realtor.com says:

"In today's market, affordability remains a key priority for homebuyers, making townhomes an attractive option because they are often priced more reasonably than single-family homes. It makes them especially appealing to first-time homebuyers on a tighter budget . . ."

So, if you're trying to buy but feeling stuck because of rising prices, shifting your focus to townhomes could be one way to get into homeownership without maxing out your budget.

Builders have seen buyers’ appetite shift to smaller homes, and they’re adjusting to meet the demand. As Joel Berner, Senior Economist at Realtor.com, explains:

"Builders are making a concerted effort to provide smaller, more affordable inventory to the market in a way that the existing-home market cannot. Townhomes are a significant portion of that effort."

And the numbers back it up. According to data from Realtor.com, townhomes now make up a bigger share of new construction listings than they did just a couple of years ago (see graph below):

That means, if you’re interested in this type of house, you have more choices than you would have had over the last few years. And more options that are potentially more affordable are definitely a good thing. It should make your search for your first home a bit easier.

That means, if you’re interested in this type of house, you have more choices than you would have had over the last few years. And more options that are potentially more affordable are definitely a good thing. It should make your search for your first home a bit easier.

If you’ve been focused only on more traditional homes with their own yards, an agent can help you explore whether a townhome could work for you. Who knows, you may find out you love the lifestyle. A lot of people do. As an article from the National Association of Realtors (NAR) explains:

“Townhomes tend to cost less than single-family detached homes and can be appealing to young professionals who may desire medium-density, walkable neighborhoods.”

That’s because they’re lower maintenance, they can provide a sense of community with other residents, and they have their own unique amenities. Not to mention, they give you the chance to start building wealth through homeownership without the upkeep that comes with having your own detached, single-family home. And that can be great for first-time buyers who are a bit worried about the maintenance anyway.

But they also come with some other considerations, like dealing with noise through shared walls. If you’re a renter right now, maybe you’re used to that already. But these are the types of things you’ll want to think about. And that’s where an agent’s expertise comes in. They’ll help you weigh the pros and cons, so you understand how a townhome fits into your lifestyle and long-term goals before making your decision.

If you're struggling to find a home within your budget, it may be time to expand your search and consider options you haven’t before, like townhomes. Sometimes, compromising a little bit on space is worth it to get your foot in the door.

What matters most to you — space, location, or budget? Connect with an agent to figure out where you can flex to make homeownership happen.

Recession talk is all over the news, and the odds of a recession are rising this year. And that leaves people wondering what would happen to the housing market if we do go into a recession.

Let’s take a look at some historical data to show what’s happened in housing for each recession going all the way back to the 1980s.

Many people think that if a recession hits, home prices will fall like they did in 2008. But that was an exception, not the rule. It was the only time we saw such a steep drop in prices. And it hasn’t happened since.

In fact, according to data from CoreLogic, in four of the last six recessions, home prices actually went up (see graph below):

So, if you’re thinking about buying or selling a home, don’t assume a recession will lead to a crash in home prices. The data simply doesn’t support that idea. Instead, home prices usually follow whatever trajectory they’re already on. And right now, nationally, home prices are still rising at a more normal pace.

While home prices tend to stay on their current path, mortgage rates usually drop during economic slowdowns. Again, looking at data from the last six recessions, mortgage rates fell each time (see graph below):

So, a recession means mortgage rates could decline based on the data. While that would help with affordability, don’t expect the return of a 3% rate.

The answer to the recession question is still unknown, but the odds have gone up. But that doesn’t mean you have to wonder about the impact on the housing market – historical data tells us what usually happens.

When you hear talk about a possible recession, what concerns or questions come to mind about buying or selling a home?

Last year, 70% of buyers abandoned their home search – and maybe you were one of them. It makes sense. Inventory was low, prices were high, and mortgage rates were up and down like a rollercoaster. All of that made it really hard to find a home you loved – and could afford.

But guess what? The market is shifting.

So, if you paused your moving plans in 2024, it might be time to hit play again. Here’s why.

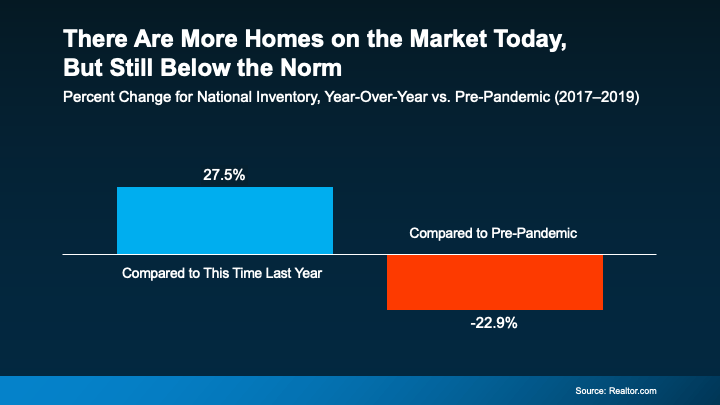

Even if you could make the numbers work, the lack of available homes in recent years probably made it hard to come by something that fit your needs. But inventory is rising, which means you have more options now.

According to Realtor.com, inventory has jumped 27.5% since this time last year (see graph below):

So, if you were reluctant to list your house because you weren’t sure where you’d go if it sold, you have more choices than you did a year ago. That’s a big win.

So, if you were reluctant to list your house because you weren’t sure where you’d go if it sold, you have more choices than you did a year ago. That’s a big win.

When the supply of homes for sale is low, they’re snatched up quickly because there just aren't enough of them to go around. And a few years ago, that meant your house could sell overnight. While that’s not always a bad thing, if you’re planning a move and also need to find your next home, a slower pace isn’t the end of the world. In fact, it’s welcome relief.

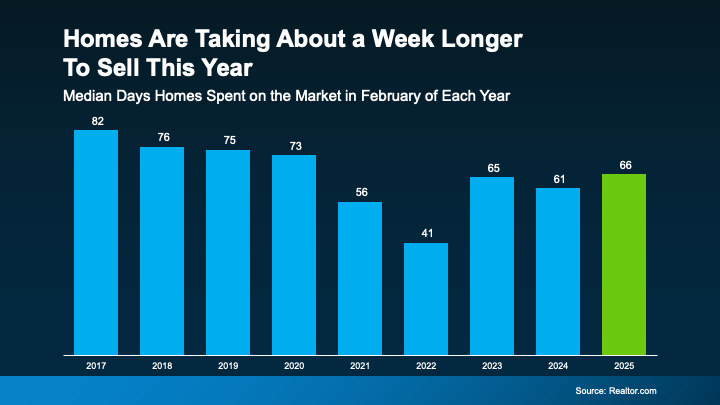

Now that inventory has grown, homes are staying on the market longer, meaning you don’t have to feel as rushed in the process (see graph below):

The latest data shows the typical time homes spent on the market went up by about 8% this year – that’s higher than we’ve seen since 2020, but still a faster pace than before the market ramped up. And it’s about a week longer than last year. Talk about a sweet spot for movers. It may seem like just a few days, but it gives you more flexibility and time to be thoughtful about your decisions. As Hannah Jones, Senior Economic Research Analyst at Realtor.com, notes:

The latest data shows the typical time homes spent on the market went up by about 8% this year – that’s higher than we’ve seen since 2020, but still a faster pace than before the market ramped up. And it’s about a week longer than last year. Talk about a sweet spot for movers. It may seem like just a few days, but it gives you more flexibility and time to be thoughtful about your decisions. As Hannah Jones, Senior Economic Research Analyst at Realtor.com, notes:

“There are more homes for sale than in the last few years, which means the market pace is a bit more manageable–with longer days on market–and many sellers are more flexible . . . Though buyers face still-high housing costs, they may find a bit more give in the market, which could give them more time to make a decision, even in the busy spring and summer months.”

And if you’re thinking – but wait – doesn’t that mean it will be harder to sell my house? Don’t worry. With inventory still almost 23% below the pre-pandemic norm, well-priced homes are selling, especially as more buyers step back into the game this season.

With growing inventory, sellers who want to upgrade, downsize, or relocate have more choices. Plus, with less pressure to rush into an offer, it could be a great time to revisit your home search if you put it on hold.

With more homes on the market and more time to make decisions, what else do you need to see in order to kickstart your home search again?