If you already own a home, have you ever stopped to think about how much wealth you’ve built up just from being a homeowner? As home values rise, so does your net worth. And, if you’ve been in your house for a few years (or longer), there’s a good chance you’re sitting on a pile of equity — maybe even more than you realize.

Home equity is the difference between what your house is worth and what you owe on your mortgage. For example, if your house is worth $500,000 and you still owe $200,000 on your home loan, you have $300,000 in equity. It’s essentially the wealth you’ve built through homeownership. Right now, homeowners across the country are seeing near-record amounts of equity.

According to the Intercontinental Exchange (ICE), the average homeowner with a mortgage has $319,000 in home equity.

The rise in equity can be credited to two key factors:

1. Significant Home Price Growth

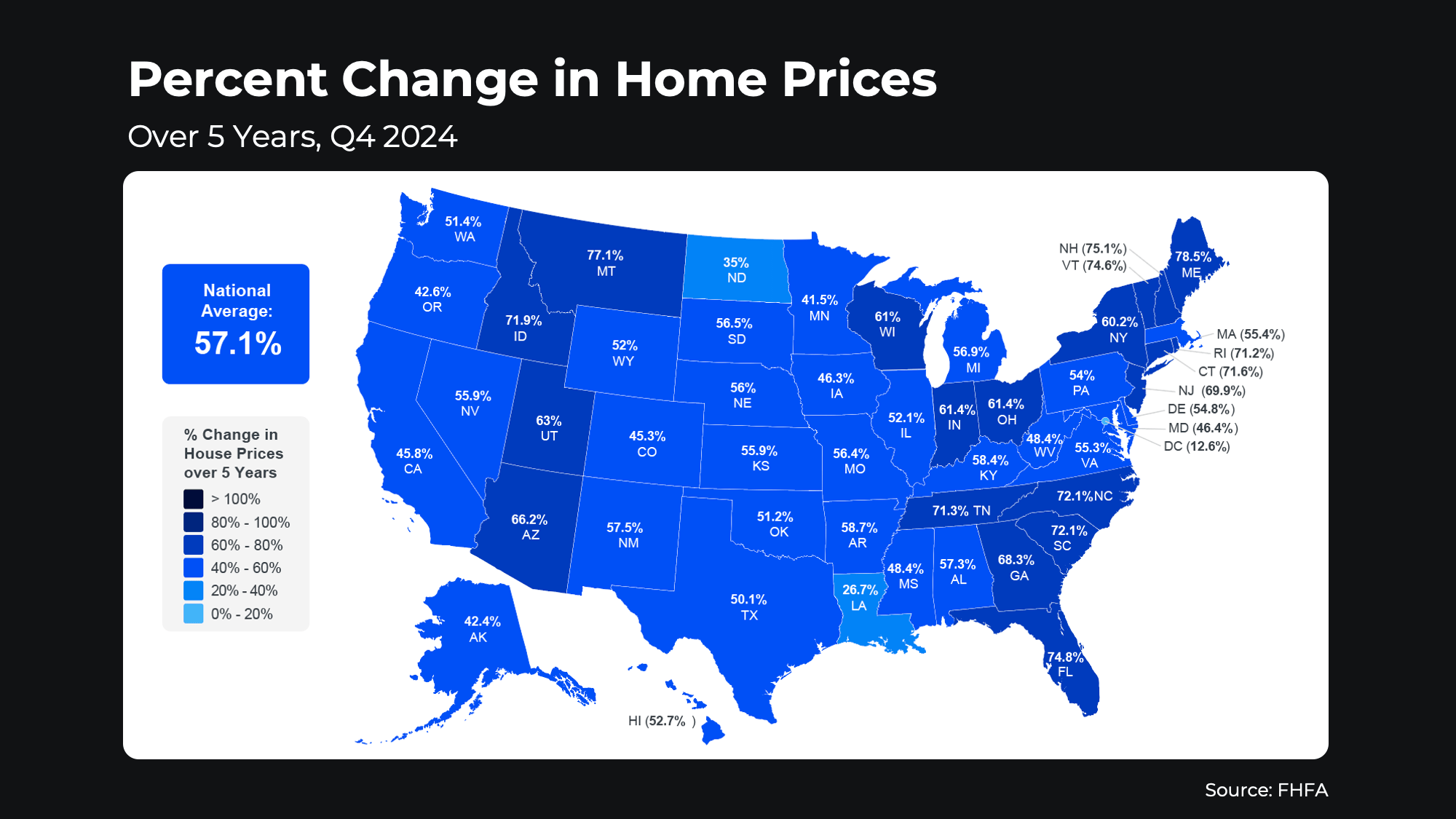

Home prices have climbed dramatically in recent years. In fact, according to the Federal Housing Finance Agency (FHFA), over the past five years, home prices nationwide have risen by 57.1% (see map below):

This appreciation means your house is likely worth much more now than when you first bought it.

This appreciation means your house is likely worth much more now than when you first bought it.

2. Longer Tenure in Homes

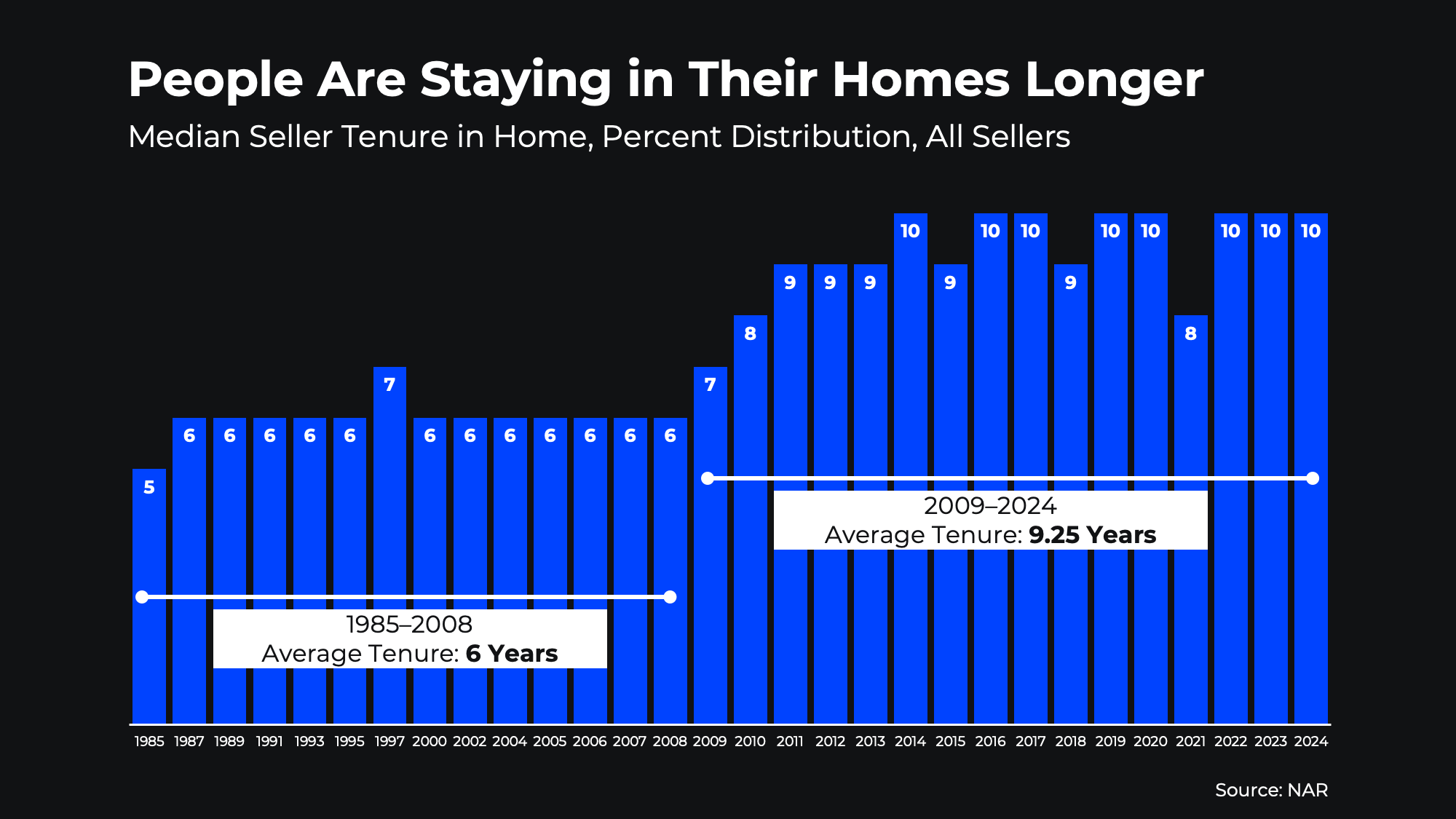

Data from the National Association of Realtors (NAR) also shows people are staying in their homes longer than they used to, with the average tenure now being close to 10 years (see graph below):

This increase means homeowners are benefiting even more from home values growing over time as they’re paying down their mortgages. That’s because the longer someone lives in their home, the more that home value grows, which directly increases equity.

This increase means homeowners are benefiting even more from home values growing over time as they’re paying down their mortgages. That’s because the longer someone lives in their home, the more that home value grows, which directly increases equity.

And if you’re one of those people who’s been in their home for 10 years or more, know this — according to NAR:

“Over the past decade, the typical homeowner has accumulated $201,600 in wealth solely from price appreciation.”

What does this mean for you? Your house might be your biggest financial asset — and it could open some exciting opportunities for your future. Let’s break it down.

Moving to Your Next Home

Your equity could help you cover the down payment for your next home. In some cases, it might even mean you can buy your next home in all cash, especially if you’re looking to downsize or move to a less expensive area.

Financing Home Improvements

Thinking about upgrading your kitchen, adding a garage or tackling other key projects? If you do it right, your equity could provide the funds to make those improvements happen, increasing the value of your home and making it more enjoyable to live in, too.

Starting a Business

If you’ve been dreaming about starting your own business, your equity could be the kickstart you need to make it happen. Whether it’s for startup costs, equipment or marketing, leveraging your home’s value could help bring your entrepreneurial goals to life while driving your long-term earning potential forward.

Fueling Your Retirement

Your home equity could be the key to funding your next chapter, too. By downsizing or moving to a more affordable area, you can unlock cash to support your retirement goals or invest in the lifestyle you’ve been hoping for — all while simplifying your living situation.

Whether you’re thinking about selling, upgrading or simply want to understand your options, your home equity is a powerful resource — and your trusted REMAX agent could help you understand exactly what you’re working with.

Want to find out how much your home is worth? Send me a quick reply, and I’ll do a professional assessment for you. The real number may surprise you.

If you already own a home, have you ever stopped to think about how much wealth you’ve built up just from being a homeowner? As home values rise, so does your net worth. And, if you’ve been in your house for a few years (or longer), there’s a good chance you’re sitting on a pile of equity — maybe even more than you realize.

Home equity is the difference between what your house is worth and what you owe on your mortgage. For example, if your house is worth $500,000 and you still owe $200,000 on your home loan, you have $300,000 in equity. It’s essentially the wealth you’ve built through homeownership. Right now, homeowners across the country are seeing near-record amounts of equity.

According to the Intercontinental Exchange (ICE), the average homeowner with a mortgage has $319,000 in home equity.

The rise in equity can be credited to two key factors:

1. Significant Home Price Growth

Home prices have climbed dramatically in recent years. In fact, according to the Federal Housing Finance Agency (FHFA), over the past five years, home prices nationwide have risen by 57.1% (see map below):

This appreciation means your house is likely worth much more now than when you first bought it.

This appreciation means your house is likely worth much more now than when you first bought it.

2. Longer Tenure in Homes

Data from the National Association of Realtors (NAR) also shows people are staying in their homes longer than they used to, with the average tenure now being close to 10 years (see graph below):

This increase means homeowners are benefiting even more from home values growing over time as they’re paying down their mortgages. That’s because the longer someone lives in their home, the more that home value grows, which directly increases equity.

This increase means homeowners are benefiting even more from home values growing over time as they’re paying down their mortgages. That’s because the longer someone lives in their home, the more that home value grows, which directly increases equity.

And if you’re one of those people who’s been in their home for 10 years or more, know this — according to NAR:

“Over the past decade, the typical homeowner has accumulated $201,600 in wealth solely from price appreciation.”

What does this mean for you? Your house might be your biggest financial asset — and it could open some exciting opportunities for your future. Let’s break it down.

Moving to Your Next Home

Your equity could help you cover the down payment for your next home. In some cases, it might even mean you can buy your next home in all cash, especially if you’re looking to downsize or move to a less expensive area.

Financing Home Improvements

Thinking about upgrading your kitchen, adding a garage or tackling other key projects? If you do it right, your equity could provide the funds to make those improvements happen, increasing the value of your home and making it more enjoyable to live in, too.

Starting a Business

If you’ve been dreaming about starting your own business, your equity could be the kickstart you need to make it happen. Whether it’s for startup costs, equipment or marketing, leveraging your home’s value could help bring your entrepreneurial goals to life while driving your long-term earning potential forward.

Fueling Your Retirement

Your home equity could be the key to funding your next chapter, too. By downsizing or moving to a more affordable area, you can unlock cash to support your retirement goals or invest in the lifestyle you’ve been hoping for — all while simplifying your living situation.

Whether you’re thinking about selling, upgrading or simply want to understand your options, your home equity is a powerful resource — and your trusted REMAX agent could help you understand exactly what you’re working with.

Want to find out how much your home is worth? Send me a quick reply, and I’ll do a professional assessment for you. The real number may surprise you.

Spring is a season of renewal, and as a homeowner, it’s easy to get swept up in the day-to-day of life. But maintaining your home is an important part of protecting the long-term value of your investment.

So, whether you own a home already or you’re planning to become a homeowner this year, here are five essential spring home maintenance tasks you don’t want to overlook. Save this as your helpful resource to come back to year after year.

Winter weather can leave behind debris, like leaves and twigs, clogging your gutters. If water can’t flow freely, it can lead to roof leaks or foundation damage. Hiring a professional to take on the height of this job is probably best, but if you’re an ace on a sturdy ladder, this may be your thing. Either way, keeping them clean and clear is a must.

Spring is the perfect time to let the sunlight in — but dirty windows can dull the view. Remove and wash your window screens, then use a window cleaner or a vinegar-water mix to make your glass sparkle. It’s a simple job that can instantly brighten your home while also keeping dirt and build-up from settling in permanently.

Spring also means it’s time to schedule a tune-up for your heating, ventilation and air conditioning system. A professional can clean and inspect your system, ensuring it’s ready to keep you cool during the summer months while also fixing any damage that may have occurred over the winter. When the summer weather heats up, you don’t want to be calling for an emergency issue that could have been prevented with regular maintenance.

After a long winter, your yard likely needs a little TLC. Rake up leaves, sticks and other debris to give your lawn room to flourish. Not only does this make your yard look tidy, but it also helps promote healthy grass growth for the warmer months ahead.

This season is a great time to touch up your home’s exterior paint and check the caulking around windows and doors. This helps prevent water damage and keeps your home looking fresh and inviting.

Owning a home is a rewarding journey, but it comes with responsibilities. By staying on top of these spring maintenance tasks, you can protect your investment and enjoy your home to the fullest. A little effort now goes a long way when it comes to keeping your home safe, efficient and beautiful for years to come.

Don’t let these essential tasks sit on the back burner. Your future self will thank you.

What’s on your to-do list this season? I’ll make sure you hit all the homeowner must-do’s and connect you to some local pros I trust who can help get the jobs done.

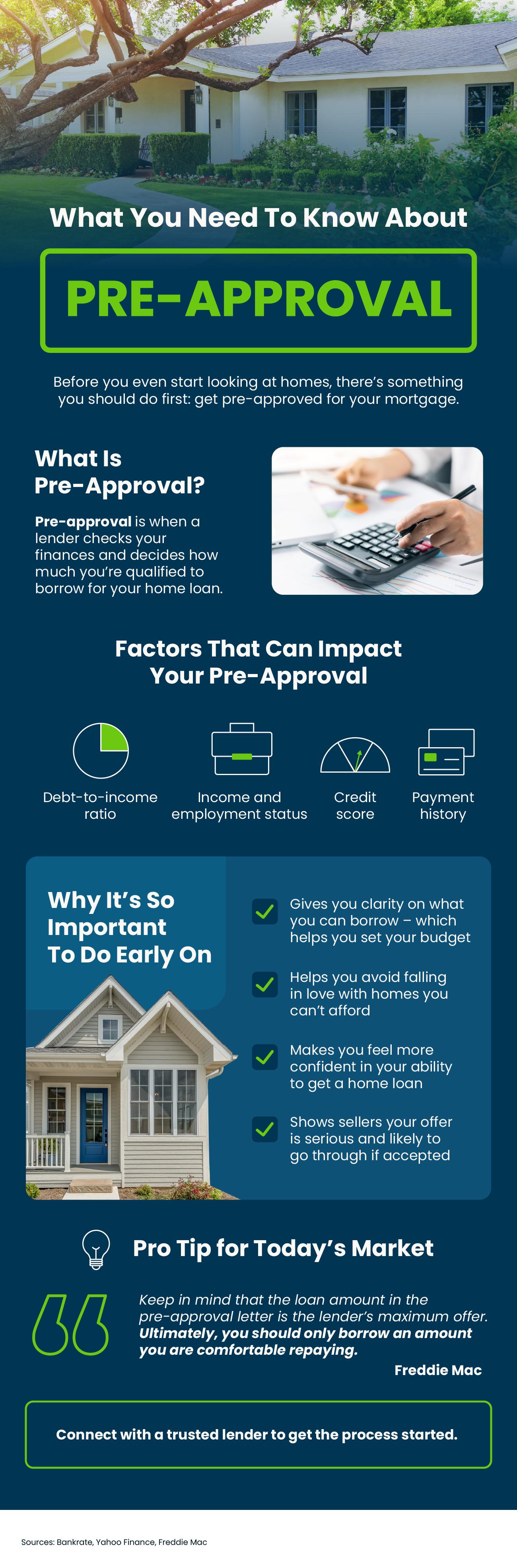

There’s one essential step in the homebuying process you may not know a whole lot about, and that’s preapproval. Here’s a rundown on what it is and why it’s so important to take care of before you start looking at homes with your REMAX® agent.

Preapproval is like getting the green light from a lender. It gives you a sense of how much they’re willing to let you borrow for your home loan. To determine that number, a lender starts by looking at your financial history. Here are some of the documents they may ask you for during this process:

The result? They’ll assess your financial situation, and you’ll get a preapproval letter showing what you can borrow. Keep in mind, any changes to your finances can affect your preapproval status. So, after you receive your letter, avoid switching jobs, applying for new credit cards or other loans, co-signing for loans or taking money from your savings.

This year, home prices are expected to rise moderately in most markets, and mortgage rates are stabilizing, but still volatile. And since affordability continues to be tight, it’s a good idea to talk to a lender about your home loan options and how today’s changing mortgage rates will impact your monthly payment.

The preapproval process is the perfect time for that discussion. Since it determines the maximum amount you can borrow, preapproval also helps you figure out your budget. And keep in mind, you may get approved for more than you feel comfortable borrowing, so use this time to decide what you can afford in your monthly mortgage payment as you factor in taxes, insurance and other costs you will incur as a homeowner. Once you know what works for you financially, partner with your REMAX agent to tailor your search to homes that match your budget. That way, you don’t fall in love with a house that’s realistically outside of your comfort zone.

Once you find a home you want to put an offer on, preapproval has another big perk. It not only makes your offer stronger, it shows sellers you’ve already undergone a credit and financial check. So, when a seller sees you’re preapproved, they view you as a much more serious buyer and may be more attracted to your offer because it is more likely to go through. And for a seller who is ready to close a deal, an offer that’s backed by preapproval makes a big difference.

As Greg McBride, Chief Financial Analyst at Bankrate, says:

“Preapproval carries more weight because it means lenders have actually done more than a cursory review of your credit and your finances, but have instead reviewed your pay stubs, tax returns and bank statements. A preapproval means you’ve cleared the hurdles necessary to be approved for a mortgage up to a certain dollar amount.”

If you’re planning on buying a home, getting preapproved for a mortgage should be one of the first things on your to-do list. Not only will it give you a better understanding of your borrowing power, it’ll put you in the best position possible to make a strong offer when you find a home you love.

Do you know what else you need to do to make sure you’re ready to buy? Reach out, and I’ll make sure you don’t skip any of the key homebuying steps.

Are you wondering what’s going on with home prices? Mortgage rates? Or asking yourself if it’s even a good time to buy a home? It’s a big decision — and you don’t have to do it alone. That’s where your trusted local REMAX® agent comes in.

For years, sellers have had the upper hand in the housing market. With so few homes for sale and so many people who wanted to purchase them, buyers faced tough competition just to get an offer accepted. But now, inventory is rising, and things are starting to shift in many areas.

So, is the market finally balancing out? And does that mean buyers will have it a bit easier now? Here’s what you need to know.

It all comes down to how many homes are for sale in an area compared to how many buyers want to buy there. That’s what ultimately determines who has the most leverage.

You can see this play out over time using data from the National Association of Realtors (NAR) in the graph below:

Where the Market Stands Now

Where the Market Stands NowWhile it’s still a seller’s market in many places, buyers in certain locations have more leverage than they’ve had in years. And that’s thanks to how much inventory has grown lately. As Lance Lambert, Co-Founder of ResiClub, explains:

"Among the nation’s 200 largest metro area housing markets, 41 markets ended January 2025 with more active homes for sale than they had in pre-pandemic January 2019. These are the places where homebuyers will be able to find the most leverage or market balance in 2025."

Here’s a look at some of the strongest seller’s markets and buyer’s markets today, according to that research:

Do you know how to adjust your plans based on who’s got the most negotiating power? Because an agent does.

Do you know how to adjust your plans based on who’s got the most negotiating power? Because an agent does.

Clever strategies can make buying in a seller’s market easier – and vice versa. And that’s exactly why you need to hire a pro. A local real estate agent knows their market like the back of their hand. They’re super familiar with what the supply and demand balance looks like and how to help their clients get a deal done either way. So, as long as you have a skilled pro by your side, it doesn’t really matter if your town is on the list or not.

With their expertise, you’ll be able to plan ahead and buy (or sell) no matter what the market looks like.

With inventory rising, the market may be starting to balance out – but it all depends on where you want to buy or sell.

If you want to know who has the most leverage where you are, talk to a local real estate agent.

If you already own a home, have you ever stopped to think about how much wealth you’ve built up just from being a homeowner? As home values rise, so does your net worth. And, if you’ve been in your house for a few years (or longer), there’s a good chance you’re sitting on a pile of equity — maybe even more than you realize.

Home equity is the difference between what your house is worth and what you owe on your mortgage. For example, if your house is worth $500,000 and you still owe $200,000 on your home loan, you have $300,000 in equity. It’s essentially the wealth you’ve built through homeownership. Right now, homeowners across the country are seeing near-record amounts of equity.

According to the Intercontinental Exchange (ICE), the average homeowner with a mortgage has $319,000 in home equity.

The rise in equity can be credited to two key factors:

1. Significant Home Price Growth

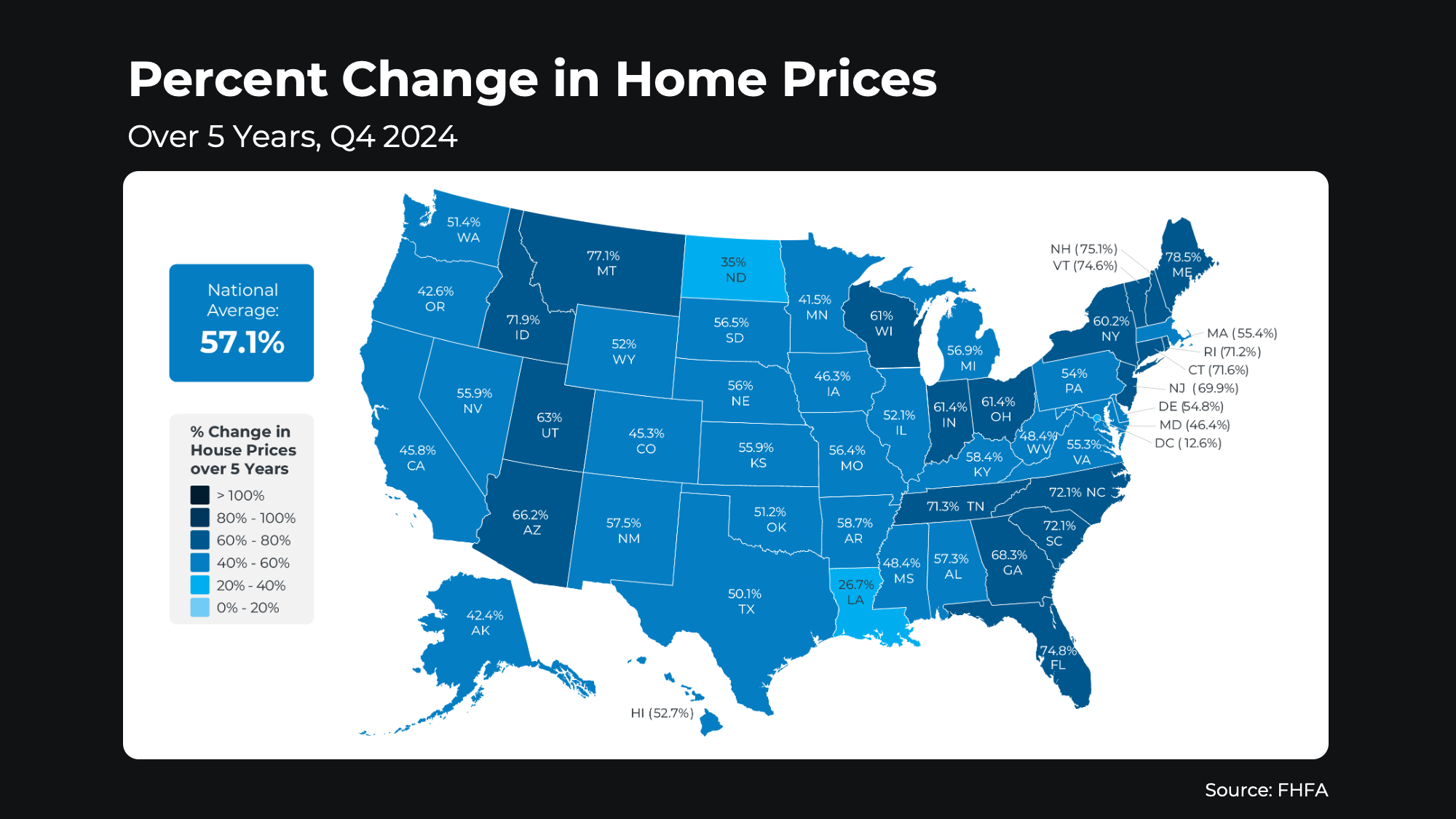

Home prices have climbed dramatically in recent years. In fact, according to the Federal Housing Finance Agency (FHFA), over the past five years, home prices nationwide have risen by 57.1% (see map below):

This appreciation means your house is likely worth much more now than when you first bought it.

2. Longer Tenure in Homes

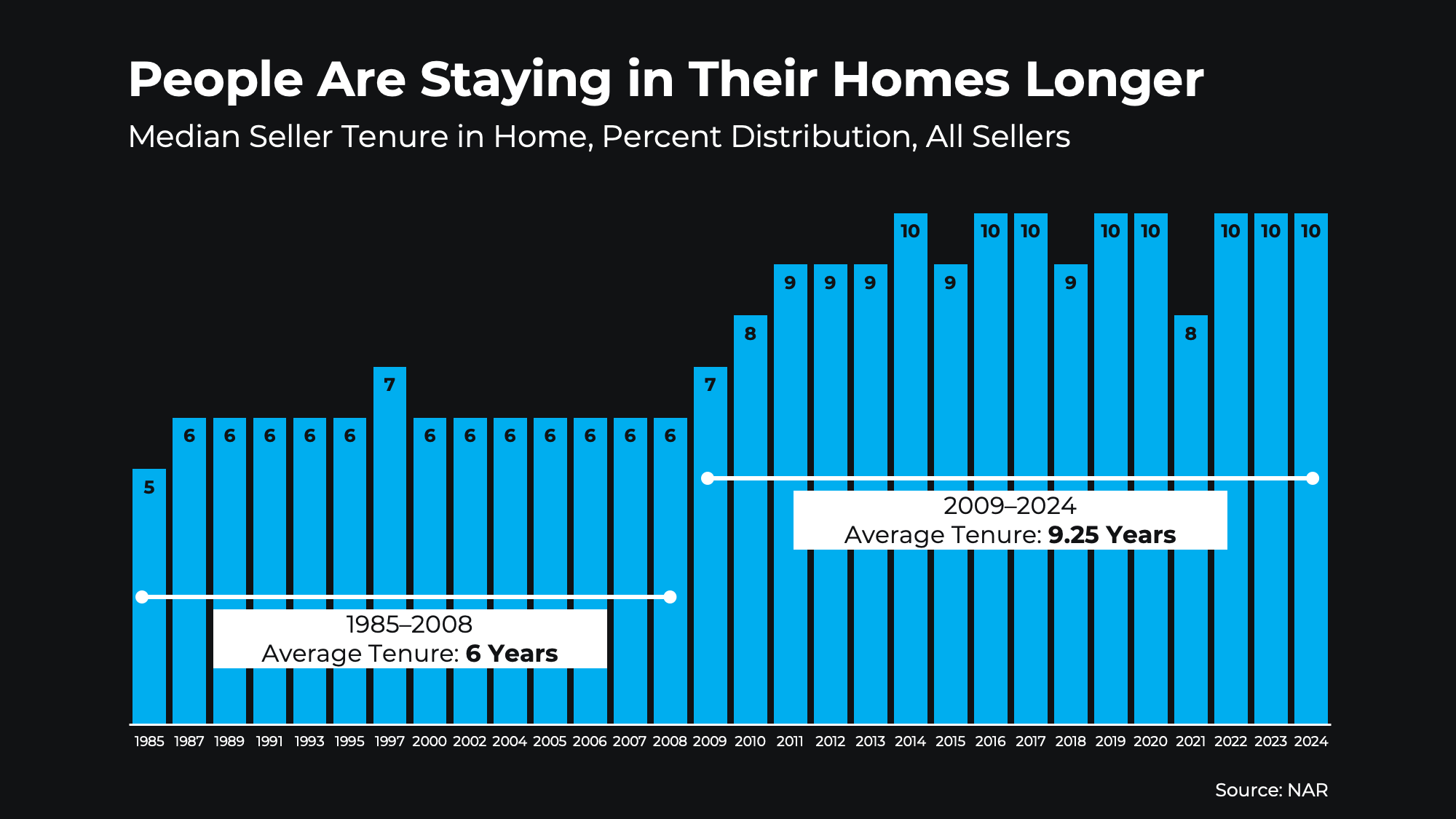

Data from the National Association of Realtors (NAR) also shows people are staying in their homes longer than they used to, with the average tenure now being close to 10 years (see graph below):

This increase means homeowners are benefiting even more from home values growing over time as they’re paying down their mortgages. That’s because the longer someone lives in their house, the more that home value grows, which directly increases equity.

And if you’re one of those people who’s been in their home for 10 years or more, know this – according to NAR:

“Over the past decade, the typical homeowner has accumulated $201,600 in wealth solely from price appreciation.”

What does this mean for you? Your house might be your biggest financial asset – and it could open some exciting opportunities for your future. Let’s break it down.

Moving to Your Next Home

Your equity could help you cover the down payment for your next home. In some cases, it might even mean you can buy your next house in all cash, especially if you’re looking to downsize or move to a less expensive area.

Financing Home Improvements

Thinking about upgrading your kitchen, adding a garage, or tackling other key projects? If you do it right, your equity can provide the funds to make those improvements happen, increasing the value of your home and making it more enjoyable to live in, too.

Starting a Business

If you’ve been dreaming about starting your own business, your equity could be the kickstart you need to make it happen. Whether it’s for startup costs, equipment, or marketing, leveraging your home’s value can help bring your entrepreneurial goals to life while driving your long-term earning potential forward.

Fueling Your Retirement

Your home equity could be the key to funding your next chapter, too. By downsizing or moving to a more affordable area, you can unlock cash to support your retirement goals or invest in the lifestyle you’ve been hoping for – all while simplifying your living situation.

Whether you’re thinking about selling, upgrading, or simply want to understand your options, your home equity is a powerful resource – and your trusted RE/MAX® agent can help you understand exactly what you’re working with.

Want to find out how much your home is worth? Send me a quick reply, and I’ll do a professional assessment for you. The real number may surprise you.

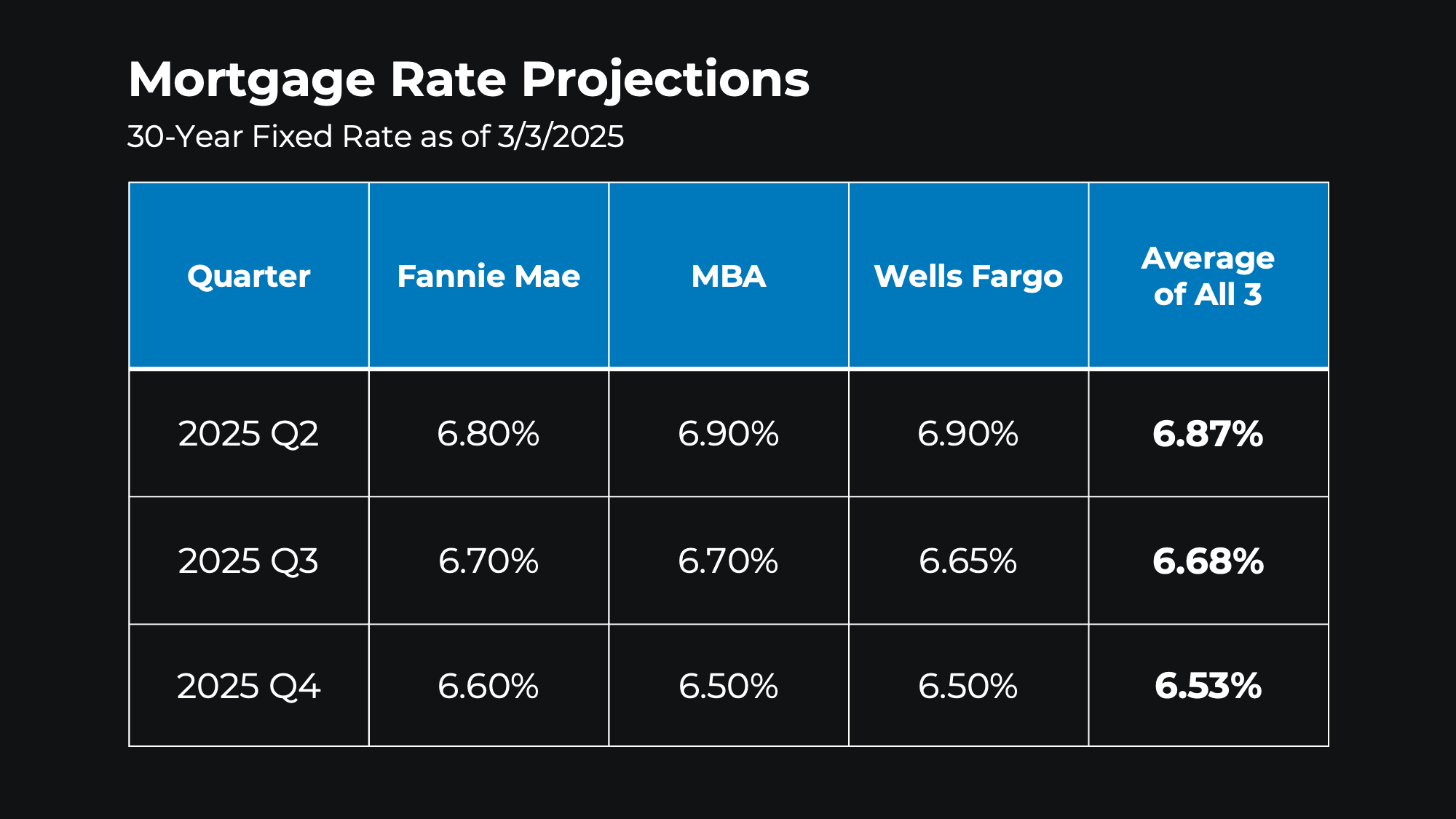

After several years of rising home prices and volatile mortgage rates, it looks like the housing market will start to head in a more normal direction in 2025 – at least according to the latest forecasts. And if you’ve been thinking about making a move, that means the uncertainty that could’ve been throwing off your plans may be coming to a close.

Here’s a look at the latest expert forecasts on two of the biggest factors expected to shape the market in the year ahead.

Everyone’s keeping an eye on mortgage rates, and they’re projected to settle in the mid-6% range by the end of the year (see chart below):

But remember, rate projections will continue to shift as new information becomes available. Expert forecasts are based on what they know right now. If there’s increasing uncertainty around inflation, employment, government policies, or other key economic drivers, mortgage rates will move. So, don’t get caught up in the exact numbers or try to time the market. Instead, focus on the fact that a bit more stability in rates isn’t a bad thing – and even a small change can help your bottom line.

But remember, rate projections will continue to shift as new information becomes available. Expert forecasts are based on what they know right now. If there’s increasing uncertainty around inflation, employment, government policies, or other key economic drivers, mortgage rates will move. So, don’t get caught up in the exact numbers or try to time the market. Instead, focus on the fact that a bit more stability in rates isn’t a bad thing – and even a small change can help your bottom line.

A trusted lender and your RE/MAX® agent will make sure you always have the latest data and the context to understand what it really means for you and your monthly payment.

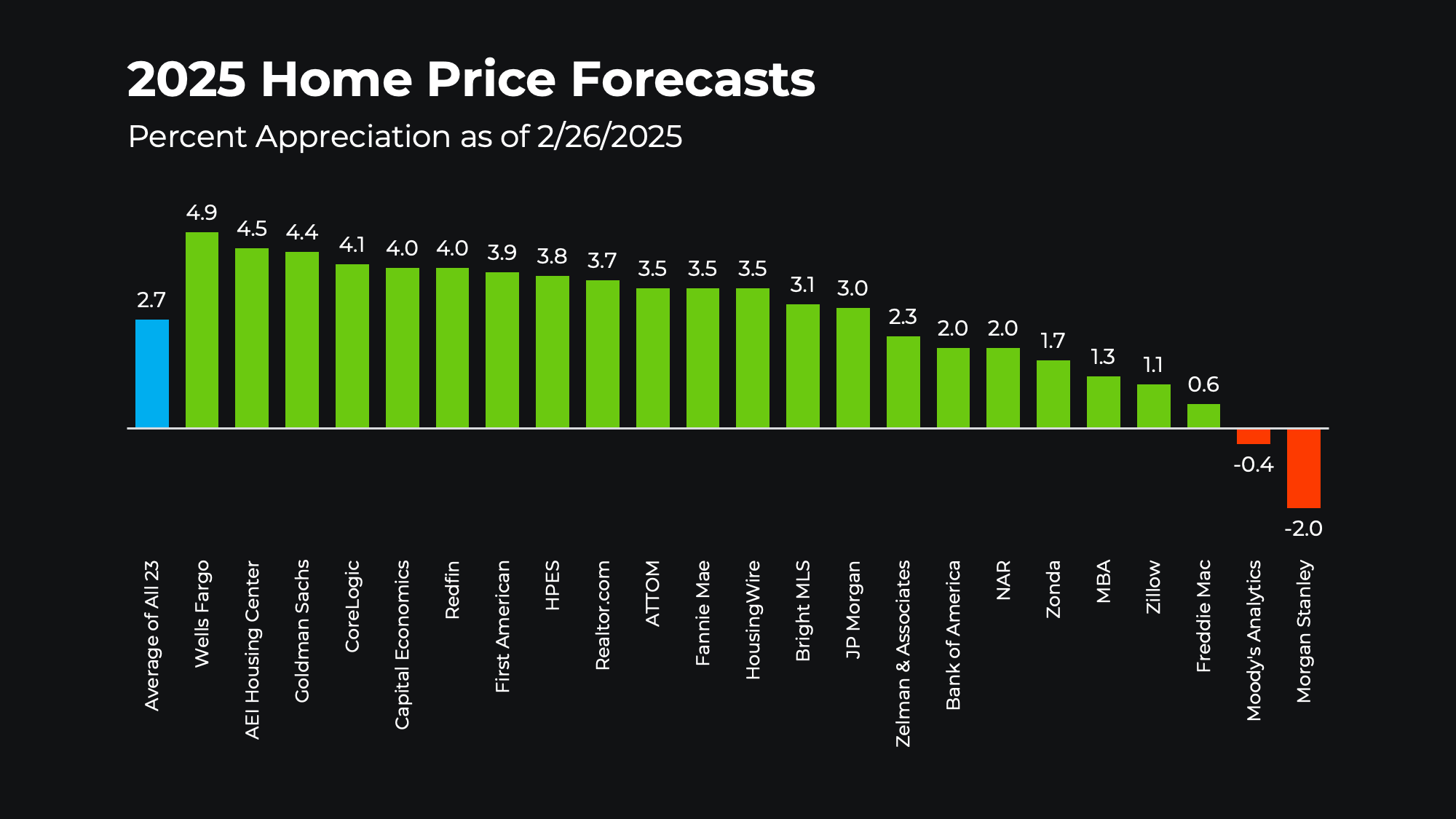

The short answer? Not likely. Home prices are projected to keep rising in most areas – just at a slower, more normal pace. If you average the expert forecasts together, you’ll see prices are expected to go up by about 2.7%, with the majority of the projections hitting somewhere in the 3 to 4% range by the end of the year. And that’s a much more typical and sustainable rise (see graph below):

So, don’t expect a sudden drop that’ll score you a big deal if you’re thinking of buying this year. While that may sound disappointing if you’re hoping prices will come down, refocus on this. It means you won’t have to deal with the steep increases the market felt in recent years, and you’ll also likely see any home you do buy go up in value after you get the keys in hand. And that’s a good thing.

So, don’t expect a sudden drop that’ll score you a big deal if you’re thinking of buying this year. While that may sound disappointing if you’re hoping prices will come down, refocus on this. It means you won’t have to deal with the steep increases the market felt in recent years, and you’ll also likely see any home you do buy go up in value after you get the keys in hand. And that’s a good thing.

Prices normalizing is a welcome sign after years of unsustainable home price growth. It means we’re moving into a healthier market. And that’s something we haven’t been able to say in a while.

And if you’re wondering how it’s even possible prices are still rising, here’s your answer. It all comes down to supply and demand. Even though there are more homes for sale now than there were just a year ago, there still aren’t enough houses on the market to keep up with all the buyers out there.

Keep in mind, though, the housing market is hyper-local. So, this will vary by area. Some markets will see even higher price appreciation. And some may see prices level off or even dip slightly. In most markets though, prices will continue to rise (as they usually do).

If you want to find out what’s happening where we live, you need to lean on your local RE/MAX® agent who can explain the latest trends and what they mean for your plans.

The housing market is shifting, and the experts say 2025 will move toward a more normal, healthier pace for the year. With rates stabilizing and home prices rising at a more typical and sustainable rate, it’s all about staying informed and making a plan that works for you.

What mortgage rate are you waiting for to make your move? Tell me your number, and I’ll show you how the math works out for your monthly mortgage payment. It may be more attainable this spring than you think.

Buying your first home is exciting, but let’s be real – it can also feel overwhelming. It’s a big step, and with that comes plenty of questions. Am I making the right decision? Can I really afford this right now? Will I be able to make ends meet if I have unexpected repairs? What if I lose my job?

Here’s the thing: every first-time homebuyer has these thoughts.

The homebuying process has always been a mix of excitement and nerves, and that’s completely normal. Here's some information that can give you a bit of perspective, so you don’t have these concerns.

Since homeownership is new to you, you’re probably feeling like it’s hard to know what to budget for. And that can be a bit scary. You’ll have the mortgage, home insurance, and maintenance to think about – maybe even lawn care or homeowner’s association (HOA) fees. It’s easy to let the dollar signs be overwhelming. As Zillow says:

“Buying a house is a big decision, and you might feel confused and indecisive as you assess your current financial situation and try to work through whether or not the timing is right. Making big life choices might come with some self-doubt, but crunching the numbers and thinking about what you want your life to look like will help guide you down the right path.”

The important thing is to focus on what you can control. By partnering with a local agent and a trusted lender, you can get a clear understanding of what you can borrow for your home loan, what your monthly payment would be, and how your mortgage rate can impact it. And since that payment will likely be your biggest recurring expense, the key is to make sure the number works for you.

The maintenance and repairs? Those can be a little bit harder to anticipate. But don’t forget you’ll get an inspection during the homebuying process to give you a better look at the condition of your future house. And with your inspection report in hand, you’ll have a good idea of what needs work. This way, you can start saving up so that you’re ready if and when something breaks.

But even then, if this is something that’s still really nagging at you, talk to your agent about asking the seller to throw in a home warranty. Those can cover repairs for some of the bigger systems in the house, like the HVAC, if they break within a specific time frame. While this isn’t a huge expense for the seller, the likelihood of a seller agreeing to one depends on what’s happening in your local market and how competitive it is right now.

And remember, chances are that money will be a little tight – at least at first. And that’s kind of to be expected. A lot of times when someone buys their first home, they cut down on things like shopping and eating out for a while until they get a better idea of how their expenses will shake out in the new home.

But if you’re crunching the numbers and you won't have enough money left for things like gas, food, etc. – it's a sign you’d be stretching yourself too far. The last thing you want is to take on a payment that’s too much to handle. But stretching a little? That’s different. That’s normal.

And don’t forget, you’ll likely earn more down the road, so that slight stretch now won’t seem so bad as time wears on. As you advance in your career, you’ll probably start to make more money too. So, as your paycheck grows, the payments will get easier. Renting is a short-term option – and it’s one you deserve to get out of. Buying a home is a long-term play.

And just in case you’re worried about what happens if you do lose your job, you should know there are options, like forbearance, designed to help you temporarily pause payments on your home loan due to hardship.

Buying your first home is a big decision, and it’s okay to feel a little nervous about it. But if you’re financially ready, don’t let fear keep you from moving forward. These emotions are normal, and great agents help their buyers get through them.

What makes you nervous when you think about buying your first home?

Connect with an agent so you have an expert on your side to explain everything along the way.